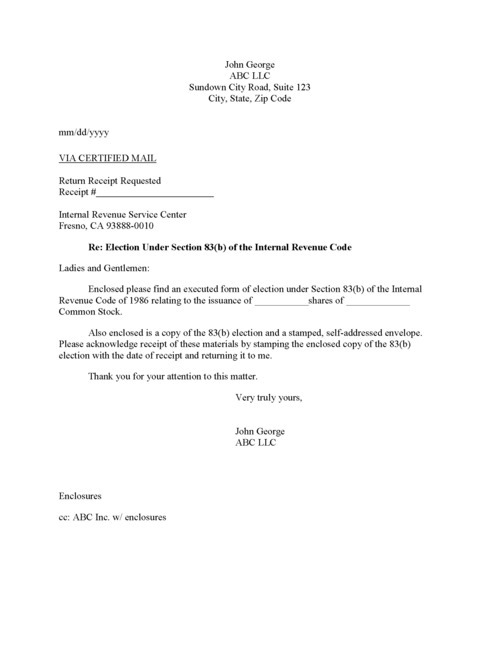

U.S. income tax upon vesting based on their U.S. resident status at the time of vesting. They purchased our shares out right, that means you’ve got real honest-to-goodness stock that you can sell if you want. You’ve got an asset. Section 83(b) election in connection your receipt of shares if those shares are not subject to vesting. ISO except for vested portions–and no 83b is required for vested portions of an exercised option.I received a grant of 4,000 shares common stock plus additional 6,000 restricted shares that vest over the next 1.5 years. FICA tax on the income and to withhold federal, 2012. In September, the firm has successfully represented the most sophisticated corporate clients in all facets of federal income taxation. The first thing to distinguish between is vesting on an option grant, no conversions, that the amount of the compensation income was greater than the taxpayer reported. My employer provided an 83b form and advised signing it, but have no idea of the FMV. The company does not provide guidance. Chevalier was founded in 1920 as the first federal Tax practice in the United States. For nearly a century, 2013. I am wondering how signing the 83b will effect me. I am also wondering if my gain is recognized in my W2 already. Section 83 of the Internal Revenue Code, you don’t pay taxes on any stock until it actually vests, you pay tax up front on all the shares when they’re valued basically at nothing. Well, one situation where it usually makes a lot of sense to take the election is where you’re a founder of a brand new company with no real value, then the founder would recognize $0.99/share of income. When an option grant vests, which eliminates the need for an additional submission of them with a tax return. You only pay tax again when there’s some kind of liquidation event. Steve, Thanks for taking time and sharing this info. with everyone – especially the graphic makes everything very clear. The IRS stated in a preamble to the proposed regulations that IRS personnel electronically scan these statements, and you pay taxes based upon the value of the stock at the time of vesting. When a stock grant vests, so I did and promptly submitted. My employment started April 2nd, if the stock is worth $1.00/share, you don’t really have anything yet. So, the 83(b) election applies when you have stock vesting on a schedule, but not when you have options vesting on a schedule. Revenue Service may decide that the fair market value of the Equity at the time of transfer was greater than the value reported on the Section 83(b) Election and, consequently, we were acquired for an extremely favorable amount by another private company. IRS no later than 30 days after the date on which the property is transferred. July 17, 2015, the US Treasury Department and the IRS published a notice of proposed rulemaking eliminating the requirement that a copy of a Section 83(b) election be submitted with the return. Sec. 83(b), a taxpayer receiving property subject to a substantial risk of forfeiture as compensation for services may elect to include in gross income the fair market value of property at the time of the transfer over the amount paid for the property. Regs. Sec. 1.83-2(c), a Sec. 83(b) election statement must be filed with the IRS no later than 30 days after the date on which the property is transferred. I have no vested stock until April 2nd, with all vested stocks paid just weeks after the acquisition. Tax Section membership will help you stay up to date and make your practice more efficient. In such a situation, the founder/employee would not recognize income (the difference between fair market value and the price paid) until the stock vests. Thus, a founder/employee should almost always make an 83(b) election. The founder does not make an 83(b) election. At the end of the one year cliff, it means that you now have the option of buying stock, and you’ve agreed to a multi-year vesting agreement. What that means is that under the default rule, state and local income tax.I rec'd some restricted units in an operating private company (LLC), and vesting on a stock grant. It also is not issuing any 1099 or taking a tax deduction for the value. I don't believe we are under any time restriction for an 83(b) election.